A Game Plan for Market Corrections

March 27, 2026

Originally published for Fidelity

Edited for clarity and brevity by Gleba & Associates

Key takeaways

- Market corrections have historically been a normal part of investing.

- While it’s natural for investors to fear the worst, historically the US market and economy have always recovered from even the steepest pullbacks.

- Fidelity’s Asset Allocation Research Team believes the US economy remains relatively strong, and is not at immediate risk of recession.

- Given the inevitability of market pullbacks, it’s important to have an investment plan you can stick with through ups and downs.

After setting new all-time highs in January, the S&P 500® Index has been declining for several weeks and nearing the threshold of a 10% drop. When major stock indexes fall by 10% or more from their peak, it’s typically considered a market correction. Some other indexes, such as the tech-heavy Nasdaq Composite and the Russell 2000 index of small companies, have already crossed into correction territory in recent days.

Corrections can occur for a variety of reasons. The market’s recent pullback has been driven by concerns around disruptions to global energy markets posed by the conflict in the Middle East, and how these disruptions may impact growth and inflation.

Corrections can be unsettling, and many investors find it difficult to stay the course when stocks are declining. But they can also present opportunities for investors. Knowing what typically drives them—and how they have tended to resolve—can help you navigate them with confidence.

How unusual are corrections?

While corrections can be unnerving, they have historically been a normal part of investing.

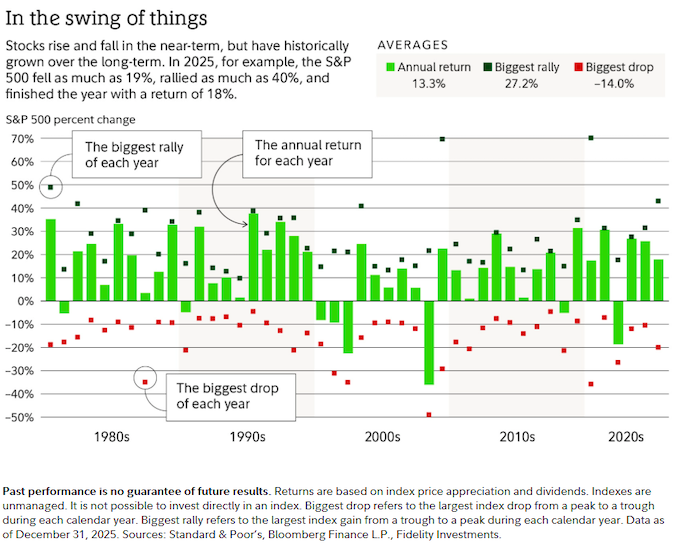

Since 1980, the S&P 500 has experienced a drop of 5% or more in 93% of calendar years, and has experienced a drop of 10% or more in 48% of calendar years.

Despite those frequent declines, the market’s average calendar-year return over the same period has been 13.3%.

How long and deep is a typical stock market correction?

It’s impossible to know how long it may take for stocks to recover their previous highs and for volatility to subside, due to the inherent unpredictability of future events.

But historically, the market has typically recovered quickly from corrections. The chart below shows the largest drop from a market high in each year (red dots). You can see that it’s not uncommon to experience significant market declines. But the market has often recovered and produced positive results in most years (shown as the green bars).

“Since 1980, the S&P 500 Index has experienced a decline of about −14% on average in any given calendar year,” says Naveen Malwal, institutional portfolio manager with Strategic Advisers, LLC, the investment manager for many of Fidelity’s managed accounts. “Yet stocks have normally recovered and finished with average gains of about 13% in any given calendar year, including dividends. So a market decline of −10% or −15% isn’t unusual, nor necessarily a sign that stocks will continue to decline. Market volatility can feel unsettling, but it is normal.”

What if this time is different?

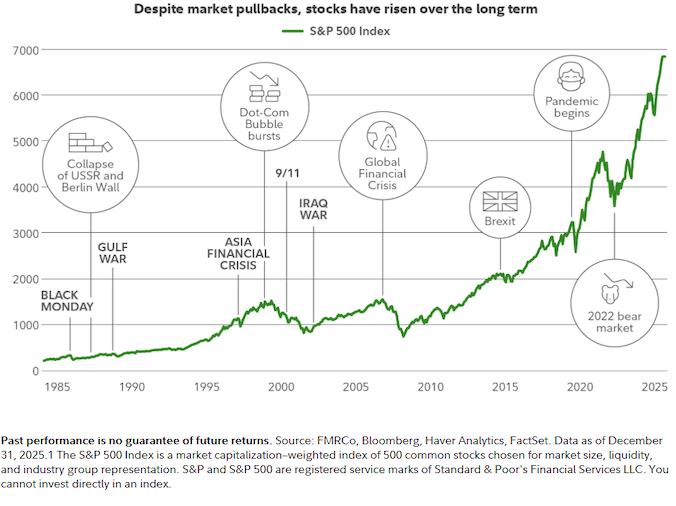

Anytime the market enters a pullback, some investors start to worry that “this time is different.” Investors should remember that historically the US economy and stock market have again and again surmounted steep obstacles—including pandemics, recessions, market bubbles, and even a depression—and eventually gone on to thrive.

“It may also help to remember that markets can react to news headlines and emotions in the short term,” says Malwal. “But over the long run, stocks have usually risen if corporate profits are growing.”

Jake Weinstein, senior vice president on Fidelity’s Asset Allocation Research Team, adds that the US economy still appears to be in the middle of an economic expansion rather than in, or on the cusp of, a recession. “Have risks increased? Yes,” Weinstein says. But the increases seen in energy prices thus far may be unlikely to single-handedly derail the US economic expansion. “Overall, the US economy is very well diversified and seems to be in a pretty good spot.”

What it means for investors

While it can take nerves of steel not to react when stocks are falling, this has often been the best course of action. Investors who sell, in an attempt to head off further losses, risk locking in potential losses and often miss out on the market’s subsequent recovery.

Here’s how to think about your potentially best course of action.

Long-term investors: Stick with your plan

If you are saving for retirement or another goal that is years away, the time to consider how much of a loss you can handle isn’t during a correction. Rather, you should consider the appropriate risk level for your portfolio when you are looking at your long-term goals, and thinking clearly about your financial situation and emotional reaction to risk.

If you haven’t created a plan, you should. If you have one, it may be worth checking in to see if your investments are still in line with that plan and if your plan continues to reflect your investment horizon, financial situation, and risk tolerance. If all that is so, you will likely be in a better position to manage the ups and downs of the market.

Retirees: Manage your income

For retirees, who may be relying on their investment portfolio for a portion of their income, a market drop can present a different kind of challenge. If you have an income plan that is built to withstand different market conditions, then you typically don’t need to react to a short-term market move. If not, it may be a good time to sit down with us to discuss your strategy.

The bottom line

It’s always impossible to know, in the moment, whether a given pullback will be short-lived or the beginning of a bigger downturn. But history shows that the stock market has eventually recovered from past downturns—even steep ones. Most sound long-term investment strategies are built to withstand volatility.

If you understand your capacity to take on risk and are comfortable with your plan, there is typically no need to take action in a correction. If you are concerned about your portfolio’s ability to weather future corrections, give us a call to discuss your plan.

https://www.fidelity.com/learning-center/trading-investing/corrections

Invest Well. Manage Well. Live Well.

Invest Well. Manage Well. Live Well. Gary is a Financial Associate at Gleba & Associates, Inc., joining our team in June 2020. After graduating from Walsh College with a Bachelor’s Degree in Finance in 2013, he began his career at Raymond James Financial Services. He then moved to the world of banking, working as a banker with Chase Private Client and then as an Assistant Vice President, Financial Advisor with PNC Investments. Gary has expertise in all aspects of financial planning including investment management, higher education planning, life insurance, and long-term care insurance needs analysis. When he gets away from the office, he loves to spend time with his wife, Lauren, and two daughters, Hadley and Harper. He enjoys woodworking, boating, summer weekends at the family cottage, spending time outdoors and traveling.

Gary is a Financial Associate at Gleba & Associates, Inc., joining our team in June 2020. After graduating from Walsh College with a Bachelor’s Degree in Finance in 2013, he began his career at Raymond James Financial Services. He then moved to the world of banking, working as a banker with Chase Private Client and then as an Assistant Vice President, Financial Advisor with PNC Investments. Gary has expertise in all aspects of financial planning including investment management, higher education planning, life insurance, and long-term care insurance needs analysis. When he gets away from the office, he loves to spend time with his wife, Lauren, and two daughters, Hadley and Harper. He enjoys woodworking, boating, summer weekends at the family cottage, spending time outdoors and traveling. Conor is a Financial Associate at Gleba & Associates, Inc., where he started in 2018. Conor has prior experience in the financial planning industry, as well as in the insurance industry. His high level of understanding insurance and financial products helps him in assessing the needs of our clients. He holds a Bachelor of Science degree in Business Administration with a concentration in Finance from the University of Detroit Mercy. You can often find Conor playing soccer or walking with his two dogs Milo, and Ellie. He is also an avid follower of the Detroit Tigers, Detroit Red Wings and his alma mater, the University of Detroit Mercy Titans.

Conor is a Financial Associate at Gleba & Associates, Inc., where he started in 2018. Conor has prior experience in the financial planning industry, as well as in the insurance industry. His high level of understanding insurance and financial products helps him in assessing the needs of our clients. He holds a Bachelor of Science degree in Business Administration with a concentration in Finance from the University of Detroit Mercy. You can often find Conor playing soccer or walking with his two dogs Milo, and Ellie. He is also an avid follower of the Detroit Tigers, Detroit Red Wings and his alma mater, the University of Detroit Mercy Titans. Lorie Heitzer is our Financial Associate at Gleba & Associates, Inc., where she has been a valuable employee for more than a decade! In her current role, Lorie assists with client reviews, implements client financial planning, and handles preparation of investment paperwork. During her time with Gleba & Associates, Lorie has earned her Series 6 (Investment Company Variable Contracts Representative), 63 (Uniform Securities Agent) and Life Insurance Licenses, allowing her to move into her current role where she assists clients in both of these areas. Lorie and her husband Bill, along with their daughters Lauren and Alexandria, and sons-in-law, Andrew & Joe, enjoy golf and make it a family event whenever possible. Her tenure at Gleba & Associates speaks volumes to her passion for the firm’s family atmosphere and her dedication to our clients and their financial and insurance needs.

Lorie Heitzer is our Financial Associate at Gleba & Associates, Inc., where she has been a valuable employee for more than a decade! In her current role, Lorie assists with client reviews, implements client financial planning, and handles preparation of investment paperwork. During her time with Gleba & Associates, Lorie has earned her Series 6 (Investment Company Variable Contracts Representative), 63 (Uniform Securities Agent) and Life Insurance Licenses, allowing her to move into her current role where she assists clients in both of these areas. Lorie and her husband Bill, along with their daughters Lauren and Alexandria, and sons-in-law, Andrew & Joe, enjoy golf and make it a family event whenever possible. Her tenure at Gleba & Associates speaks volumes to her passion for the firm’s family atmosphere and her dedication to our clients and their financial and insurance needs. Terri is the Service Manager at Gleba & Associates, Inc., Joining the team in April, 2015. In her role, she handles client service requests and underwriting. Terri’s previous experience in 401(k) Retirement Plans, Payroll and Human Resource Administration is invaluable, allowing Gleba & Associates to grow and run efficiently. This is knowledge that can also assist our small business clients as they grow their businesses. Terri enjoys spending time with family, which includes her husband, Gerry and her two children, Vincent and Genna. She loves the outdoors and camping with family in their RV. Terri looks forward to continuing the high level of customer service you have come to expect from Gleba & Associates!

Terri is the Service Manager at Gleba & Associates, Inc., Joining the team in April, 2015. In her role, she handles client service requests and underwriting. Terri’s previous experience in 401(k) Retirement Plans, Payroll and Human Resource Administration is invaluable, allowing Gleba & Associates to grow and run efficiently. This is knowledge that can also assist our small business clients as they grow their businesses. Terri enjoys spending time with family, which includes her husband, Gerry and her two children, Vincent and Genna. She loves the outdoors and camping with family in their RV. Terri looks forward to continuing the high level of customer service you have come to expect from Gleba & Associates! Michael is the Marketing Manager at Gleba & Associates, Inc., where he began in August 2017. In his position, Michael creates and develops marketing strategies to enhance the image of Gleba & Associates, and helps maximize the Client-Advisor relationship. He is also in charge of company events, seminars, and educational workshops. Michael has a Bachelor of Applied Arts Degree in Integrative Public Relations from Central Michigan University. When he is not in the office, Michael can most likely be found playing billiards, playing poker, on the tennis court, or rooting on the Utica Unicorns baseball team. Michael stays active by going to the gym and going to the dog park with his Labrador-mix, Milton. His approachable attitude, along with experience in marketing, communications, and social media, makes him a valuable asset to the Gleba & Associates team.

Michael is the Marketing Manager at Gleba & Associates, Inc., where he began in August 2017. In his position, Michael creates and develops marketing strategies to enhance the image of Gleba & Associates, and helps maximize the Client-Advisor relationship. He is also in charge of company events, seminars, and educational workshops. Michael has a Bachelor of Applied Arts Degree in Integrative Public Relations from Central Michigan University. When he is not in the office, Michael can most likely be found playing billiards, playing poker, on the tennis court, or rooting on the Utica Unicorns baseball team. Michael stays active by going to the gym and going to the dog park with his Labrador-mix, Milton. His approachable attitude, along with experience in marketing, communications, and social media, makes him a valuable asset to the Gleba & Associates team. Moiz is our Financial Associate at Gleba & Associates, Inc., where he began in 2013 after working for Bank of America and Thomson Reuters in various financial roles. In his position, Moiz assists in the research of financial solutions in order to meet client’s needs, conducts client reviews, provides insurance quotes, offers detailed financial plans, and delivers follow-up services to our clients. Before moving to the United States in 2004, Moiz grew up in rural India, where he was raised in a family of entrepreneurs. This allowed him to quickly learn the value of financial investment. Moiz holds a Bachelor of Commerce Degree in Accounting from Gujrat University and a B.B.A. in Management and an MBA from Walsh College of Accountancy and Business Administration, where he was elected as a member of Delta Mu Delta, the International Honor Society in Business Administration in recognition of high scholastic attainment. Moiz enjoys spending time with his wife, Tasneem, son, Taha, and family. He also loves playing tennis and rebuilding computers. His expertise in the areas of banking, mortgage and taxation helps to provide our clients with distinct portfolio advice as well as overall financial direction and growth.

Moiz is our Financial Associate at Gleba & Associates, Inc., where he began in 2013 after working for Bank of America and Thomson Reuters in various financial roles. In his position, Moiz assists in the research of financial solutions in order to meet client’s needs, conducts client reviews, provides insurance quotes, offers detailed financial plans, and delivers follow-up services to our clients. Before moving to the United States in 2004, Moiz grew up in rural India, where he was raised in a family of entrepreneurs. This allowed him to quickly learn the value of financial investment. Moiz holds a Bachelor of Commerce Degree in Accounting from Gujrat University and a B.B.A. in Management and an MBA from Walsh College of Accountancy and Business Administration, where he was elected as a member of Delta Mu Delta, the International Honor Society in Business Administration in recognition of high scholastic attainment. Moiz enjoys spending time with his wife, Tasneem, son, Taha, and family. He also loves playing tennis and rebuilding computers. His expertise in the areas of banking, mortgage and taxation helps to provide our clients with distinct portfolio advice as well as overall financial direction and growth.