Originally written by Jared Franz, Gerald Du Manoir, Chris Buchbinder, John Queen and Steve Watson

Originally written for Capital Group

August 5, 2024

With global equity markets selling off sharply in the first few days of August, investor sentiment has quickly shifted from exuberance to apprehension. Concerns about softening U.S. economic growth, high interest rates and technology sector valuations have combined to shake confidence in a market that was previously priced for perfection.

At such times of stress in the markets, it’s important to take a step back, review the fundamentals, and determine whether the current volatility is perhaps an overreaction or an expected correction after a long stretch of strong returns.

Here are five views from Capital Group investment professionals assessing the latest, fast-changing market developments.

Macro view remains positive

Jared Franz, U.S. economist

We’re in the summer season where market liquidity is low and so markets generally overshoot based on positive and negative news. That’s unlikely to change in the next few weeks so I’d expect more volatility to come.

On the economic side I’m not seeing anything in the data that would suggest a sharp drop-off or a change in the fundamentals of the U.S. economy. Most of what I’m seeing is a slump in the pace of economic activity, but not necessarily a contraction.

A flagging economy is generally consistent with weakening labor markets and wages, which have the effect of slowing the pace of consumption. That said, if we continue to see economic data weakening across the board, consistent with U.S. unemployment rising above 4.5% to 5.0%, I think that would lay the groundwork for more interest rate cuts from the U.S. Federal Reserve than the market has priced in right now. Another key change and difference versus three to six months ago is the pace of economic activity in Europe and China, which has been much slower of late.

Global equity markets have experienced a strong run-up until now

Even with a modestly slowing economy, U.S. corporate earnings have been robust. Overall, equity markets remain reasonably priced with the S&P 500 Index trading at a multiple of 20.8 times 12-month forward earnings, and even the Magnificent Seven (ex-Tesla) at 27.8 times, as of August 2. And even though the market selloff has been at least partly triggered by worry that the Fed may be behind the curve in lowering rates, the fact is that we are at the beginning of an easing cycle with both nominal and real interest rates that are not exceedingly high by historical standards.

Taken altogether, this feels more like a serious pocket of turbulence rather than a full-blown contraction.

Equity markets were primed for a fall

Gerald Du Manoir, equity portfolio manager

We have witnessed a period of hyper-concentration where the market was suggesting that only a few companies deserved to be trading at higher multiples. Investors were very focused on themes. Going forward, I expect the market to be more focused on company fundamentals, regardless of the theme, whether it is artificial intelligence (AI) or weight loss drugs, or value or growth.

In the last few years, a number of solid companies’ valuations compressed as the market focused on tech and AI. Many of those companies have held up relatively well recently. I think this correction is telling us is that, going forward, it will be crucial to focus on company fundamentals. A balanced and diversified approach will be essential. And, eventually, the fundamentals will reassert themselves.

AI entering a zone of disillusionment

Chris Buchbinder, equity portfolio manager

A correction in AI-related stocks was to be expected. There has been a great amount of enthusiasm around AI, just as there was around the internet in 2000. I think AI is absolutely real and will change all of our lives in dramatic ways over the next five to 10 years. But I also think we are entering a zone of disillusionment. With any growth trend, there is a period when fundamentals may slow, and while they may end up being great over the long term, you can get extreme reactions in the market.

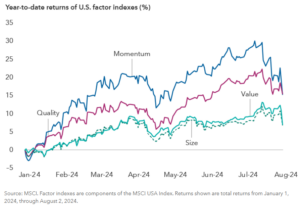

Indeed, while the recent equity market selloff has been swift and powerful, it has been most acute among so-called momentum stocks, or stocks whose share prices have been trending in one direction for a period. Many dividend payers and quality companies, or those companies with visible near-term cash flow generation, have held up relatively well.

Momentum stocks have taken the brunt of the selloff

Bonds holding up amid stock market plunge

John Queen, fixed income portfolio manager

Rates markets offered some respite during this broad equity downturn, as U.S. Treasuries rallied significantly in reaction to Friday’s jobs report. Investors seeking shelter amid heightened recession fears pushed Treasury yields down significantly last week, while equities fell and credit spreads widened. (Bond yields move inversely to prices.)

These market moves follow a weaker-than-expected payroll report on Friday showing slower job growth and an unemployment rate that rose to 4.3% from 4.1% in June, triggering the Sahm Rule, which states that such a rise in the unemployment rate from a trough has never occurred without a recession. Last week, the Fed held rates steady at a range of 5.25% to 5.50% for the eighth consecutive time. Fed chair Jerome Powell signaled that cuts could come as soon as September, but markets are questioning whether a standard 25-basis-point reduction will be too little too late.

With higher starting yields across the curve, bonds have often been able to do what they are meant to do when equities sell off. The negative correlation between bonds and stocks as shown last week serves as a reminder of the importance of diversification and the role of fixed income in investors’ portfolios.

Friday’s job numbers continued to show moderation and might show us on a path to real weakness and recession, but it is not clear we are on one yet. Given the violent swings we have seen year to date due to individual economic data releases and market expectations for rate cuts, we believe it is prudent to remain forward-looking and focused on the bigger picture when identifying the right time to adjust positions.

Japan provided initial sparks for global selloff

Steve Watson, equity portfolio manager

A spike in the value of the Japanese yen may also be contributing to market volatility in the U.S. Last week, the Bank of Japan surprised markets by raising its benchmark interest rate 15 basis points to 0.25% — its highest level since the global financial crisis — and announced a plan to pare back its quantitative easing program. This led the yen to appreciate significantly against the U.S. dollar.

The impact has been felt by Japanese equity markets, which fell sharply, and it could be filtering through to the U.S. The yen has been a currency of choice for many investors executing so-called carry trades, in which they borrow in a low-yielding currency to invest in other higher yielding currencies or assets. With the yen rebounding dramatically, investors in these trades could be selling other assets, including U.S. stocks, to find liquidity to cover their losses and fund capital calls. However, it is difficult to quantify the magnitude of any such effect.

Some would say that the recent strength of the Japanese yen has caused investors in Japan to shift out of the Magnificent Seven stocks, which has led the U.S. market down. Perhaps so. But I’d say a more probable answer is that U.S.-listed growth stocks just got too expensive and now need some time to correct.

Meanwhile, Japanese stocks have rallied over the past year on expectations of improving fundamentals. Companies have come under pressure from regulators to improve overall financial health, leading many to dispose of non-core businesses. Against this backdrop, some investors worry that Japan’s central bank may have tightened policy too soon.

Original article: https://www.capitalgroup.com/advisor/insights/articles/5-views-on-tumbling-markets.html

Invest Well. Manage Well. Live Well.

Invest Well. Manage Well. Live Well. Gary is a Financial Associate at Gleba & Associates, Inc., joining our team in June 2020. After graduating from Walsh College with a Bachelor’s Degree in Finance in 2013, he began his career at Raymond James Financial Services. He then moved to the world of banking, working as a banker with Chase Private Client and then as an Assistant Vice President, Financial Advisor with PNC Investments. Gary has expertise in all aspects of financial planning including investment management, higher education planning, life insurance, and long-term care insurance needs analysis. When he gets away from the office, he loves to spend time with his wife, Lauren, and two daughters, Hadley and Harper. He enjoys woodworking, boating, summer weekends at the family cottage, spending time outdoors and traveling.

Gary is a Financial Associate at Gleba & Associates, Inc., joining our team in June 2020. After graduating from Walsh College with a Bachelor’s Degree in Finance in 2013, he began his career at Raymond James Financial Services. He then moved to the world of banking, working as a banker with Chase Private Client and then as an Assistant Vice President, Financial Advisor with PNC Investments. Gary has expertise in all aspects of financial planning including investment management, higher education planning, life insurance, and long-term care insurance needs analysis. When he gets away from the office, he loves to spend time with his wife, Lauren, and two daughters, Hadley and Harper. He enjoys woodworking, boating, summer weekends at the family cottage, spending time outdoors and traveling. Conor is a Financial Associate at Gleba & Associates, Inc., where he started in 2018. Conor has prior experience in the financial planning industry, as well as in the insurance industry. His high level of understanding insurance and financial products helps him in assessing the needs of our clients. He holds a Bachelor of Science degree in Business Administration with a concentration in Finance from the University of Detroit Mercy. You can often find Conor playing soccer or walking with his two dogs Milo, and Ellie. He is also an avid follower of the Detroit Tigers, Detroit Red Wings and his alma mater, the University of Detroit Mercy Titans.

Conor is a Financial Associate at Gleba & Associates, Inc., where he started in 2018. Conor has prior experience in the financial planning industry, as well as in the insurance industry. His high level of understanding insurance and financial products helps him in assessing the needs of our clients. He holds a Bachelor of Science degree in Business Administration with a concentration in Finance from the University of Detroit Mercy. You can often find Conor playing soccer or walking with his two dogs Milo, and Ellie. He is also an avid follower of the Detroit Tigers, Detroit Red Wings and his alma mater, the University of Detroit Mercy Titans. Lorie Heitzer is our Financial Associate at Gleba & Associates, Inc., where she has been a valuable employee for more than a decade! In her current role, Lorie assists with client reviews, implements client financial planning, and handles preparation of investment paperwork. During her time with Gleba & Associates, Lorie has earned her Series 6 (Investment Company Variable Contracts Representative), 63 (Uniform Securities Agent) and Life Insurance Licenses, allowing her to move into her current role where she assists clients in both of these areas. Lorie and her husband Bill, along with their daughters Lauren and Alexandria, and sons-in-law, Andrew & Joe, enjoy golf and make it a family event whenever possible. Her tenure at Gleba & Associates speaks volumes to her passion for the firm’s family atmosphere and her dedication to our clients and their financial and insurance needs.

Lorie Heitzer is our Financial Associate at Gleba & Associates, Inc., where she has been a valuable employee for more than a decade! In her current role, Lorie assists with client reviews, implements client financial planning, and handles preparation of investment paperwork. During her time with Gleba & Associates, Lorie has earned her Series 6 (Investment Company Variable Contracts Representative), 63 (Uniform Securities Agent) and Life Insurance Licenses, allowing her to move into her current role where she assists clients in both of these areas. Lorie and her husband Bill, along with their daughters Lauren and Alexandria, and sons-in-law, Andrew & Joe, enjoy golf and make it a family event whenever possible. Her tenure at Gleba & Associates speaks volumes to her passion for the firm’s family atmosphere and her dedication to our clients and their financial and insurance needs. Terri is the Service Manager at Gleba & Associates, Inc., Joining the team in April, 2015. In her role, she handles client service requests and underwriting. Terri’s previous experience in 401(k) Retirement Plans, Payroll and Human Resource Administration is invaluable, allowing Gleba & Associates to grow and run efficiently. This is knowledge that can also assist our small business clients as they grow their businesses. Terri enjoys spending time with family, which includes her husband, Gerry and her two children, Vincent and Genna. She loves the outdoors and camping with family in their RV. Terri looks forward to continuing the high level of customer service you have come to expect from Gleba & Associates!

Terri is the Service Manager at Gleba & Associates, Inc., Joining the team in April, 2015. In her role, she handles client service requests and underwriting. Terri’s previous experience in 401(k) Retirement Plans, Payroll and Human Resource Administration is invaluable, allowing Gleba & Associates to grow and run efficiently. This is knowledge that can also assist our small business clients as they grow their businesses. Terri enjoys spending time with family, which includes her husband, Gerry and her two children, Vincent and Genna. She loves the outdoors and camping with family in their RV. Terri looks forward to continuing the high level of customer service you have come to expect from Gleba & Associates! Michael is the Marketing Manager at Gleba & Associates, Inc., where he began in August 2017. In his position, Michael creates and develops marketing strategies to enhance the image of Gleba & Associates, and helps maximize the Client-Advisor relationship. He is also in charge of company events, seminars, and educational workshops. Michael has a Bachelor of Applied Arts Degree in Integrative Public Relations from Central Michigan University. When he is not in the office, Michael can most likely be found playing billiards, playing poker, on the tennis court, or rooting on the Utica Unicorns baseball team. Michael stays active by going to the gym and going to the dog park with his Labrador-mix, Milton. His approachable attitude, along with experience in marketing, communications, and social media, makes him a valuable asset to the Gleba & Associates team.

Michael is the Marketing Manager at Gleba & Associates, Inc., where he began in August 2017. In his position, Michael creates and develops marketing strategies to enhance the image of Gleba & Associates, and helps maximize the Client-Advisor relationship. He is also in charge of company events, seminars, and educational workshops. Michael has a Bachelor of Applied Arts Degree in Integrative Public Relations from Central Michigan University. When he is not in the office, Michael can most likely be found playing billiards, playing poker, on the tennis court, or rooting on the Utica Unicorns baseball team. Michael stays active by going to the gym and going to the dog park with his Labrador-mix, Milton. His approachable attitude, along with experience in marketing, communications, and social media, makes him a valuable asset to the Gleba & Associates team. Moiz is our Financial Associate at Gleba & Associates, Inc., where he began in 2013 after working for Bank of America and Thomson Reuters in various financial roles. In his position, Moiz assists in the research of financial solutions in order to meet client’s needs, conducts client reviews, provides insurance quotes, offers detailed financial plans, and delivers follow-up services to our clients. Before moving to the United States in 2004, Moiz grew up in rural India, where he was raised in a family of entrepreneurs. This allowed him to quickly learn the value of financial investment. Moiz holds a Bachelor of Commerce Degree in Accounting from Gujrat University and a B.B.A. in Management and an MBA from Walsh College of Accountancy and Business Administration, where he was elected as a member of Delta Mu Delta, the International Honor Society in Business Administration in recognition of high scholastic attainment. Moiz enjoys spending time with his wife, Tasneem, son, Taha, and family. He also loves playing tennis and rebuilding computers. His expertise in the areas of banking, mortgage and taxation helps to provide our clients with distinct portfolio advice as well as overall financial direction and growth.

Moiz is our Financial Associate at Gleba & Associates, Inc., where he began in 2013 after working for Bank of America and Thomson Reuters in various financial roles. In his position, Moiz assists in the research of financial solutions in order to meet client’s needs, conducts client reviews, provides insurance quotes, offers detailed financial plans, and delivers follow-up services to our clients. Before moving to the United States in 2004, Moiz grew up in rural India, where he was raised in a family of entrepreneurs. This allowed him to quickly learn the value of financial investment. Moiz holds a Bachelor of Commerce Degree in Accounting from Gujrat University and a B.B.A. in Management and an MBA from Walsh College of Accountancy and Business Administration, where he was elected as a member of Delta Mu Delta, the International Honor Society in Business Administration in recognition of high scholastic attainment. Moiz enjoys spending time with his wife, Tasneem, son, Taha, and family. He also loves playing tennis and rebuilding computers. His expertise in the areas of banking, mortgage and taxation helps to provide our clients with distinct portfolio advice as well as overall financial direction and growth.